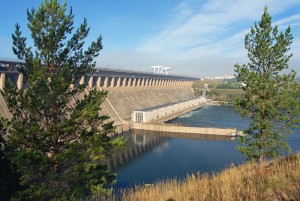

Hydroelectric power plants – gigantic dams across the country’s biggest rivers that supply cheap energy to entire Russian regions and their extremely energy-intensive industrial enterprises – used to be one of the key symbols of the Soviet Union’s industrial might. Up to this day, Russia’s hydroelectric power plants have been cumulatively providing around 20 percent of the country’s energy.

Out of more than 100 major hydroelectric power plants, with the total number of them in Russia reaching almost 200, most are owned by RusHydro PJSC that was founded as a public company by chief architect of the Russian privatization, Anatoli Chubais. However, the state still owns 67 percent of the company’s shares. Another three major hydroelectric power plants belong to En+ Group controlled by Oleg Deripaska who is also president of the world’s second largest aluminum company Rusal. Deripaska’s interest toward hydroelectric power industry is not surprising since aluminum production is a highly energy-consuming process, and Rusal uses most of the electricity generated by Deripaska’s hydroelectric plants. Deripaska’s Russian assets can be considered private only nominally. A classic Russian oligarch of the 1990s, Deripaska is well-known for a statement he made in his 2007 interview to the Financial Times: “If the state says we need to give it up, we’ll give it up. I don’t separate myself from the state. I have no other interests.” Since in recent years global demand for aluminum has been steadily decreasing, Deripaska has no plans to extend his energy assets. As to the situation with RusHydro, its future is less clear. What is obvious that it shows much more signs of corruption and lack of professionalism. Read More “Hydroelectric Power in Service of Cooperative Ozero”